The realization that centralized cloud infrastructures cannot support the instantaneous decision-making required by autonomous systems has fundamentally rewritten the blueprint for modern vision hardware development. As the industry moves deeper into 2026, the transition from experimental AI to ubiquitous edge intelligence is no longer a forecast but an operational reality across the global supply chain. This shift necessitates a new class of silicon that prioritizes high-throughput data processing and low-power consumption over the raw, unrefined horsepower of traditional data center CPUs. To meet these demands, hardware accelerators are evolving into highly specialized devices that can interpret visual data in microseconds, providing the “eyes” for everything from surgical robots to high-speed sorting machines. This evolution is not merely a technical upgrade; it represents a philosophical change in how machines perceive their environment, moving from reactive recording to proactive, real-time analysis that happens at the very point of capture. As we look toward the next decade, the convergence of vision sensors and dedicated neural processing units will likely redefine the limits of automation, turning what were once static cameras into intelligent decision-makers that operate independently of a constant internet connection.

Economic Growth and the Migration to the Edge

Projections for Market Value: A Decade of Sustained Expansion

The financial trajectory for the vision hardware sector indicates a robust and steady expansion, with a compound annual growth rate projected to hold near ten percent through 2035. This sustained climb suggests that the market value will more than double over the coming decade, reflecting how deeply vision technology has been integrated into the foundational layers of the global economy. Unlike previous hype cycles driven by consumer gadgets, this current growth phase is anchored in “sticky” industrial and commercial applications that remain resilient even during periods of broader economic fluctuation. Companies are no longer viewing vision accelerators as optional high-tech luxuries but as essential components required to maintain a competitive edge in productivity and quality control. This transition is particularly evident in the way capital expenditure is being redirected from general-purpose server upgrades toward specialized edge devices that can deliver immediate returns on investment through labor savings and error reduction.

Structural shifts in smart manufacturing and autonomous logistics are the primary engines behind this financial surge, creating a market environment where high-end vision acceleration is a non-negotiable expense. As the world sees a continued rise in global GDP and a gradual easing of the fabrication bottlenecks that plagued the early 2020s, the hardware ecosystem is better positioned than ever to achieve high levels of technological sophistication. Investors are increasingly focusing on firms that produce the silicon necessary for semiconductor inspection and automated warehouse management, recognizing that these sectors provide a stable floor for demand. This economic stability allows semiconductor manufacturers to invest more heavily in research and development for the next generation of 2nm and 1nm chips, ensuring that the hardware available by 2035 will be exponentially more capable than the solutions currently deployed. The maturation of these procurement channels ensures that the vision hardware industry will remain a cornerstone of the broader technology market for the foreseeable future.

The Rise of Edge Inference: Custom Silicon and Neural Processing

A monumental shift is currently occurring as processing power migrates from centralized cloud servers directly to the sensor node, a movement commonly referred to as the Edge AI revolution. By processing visual data at the exact point of capture, systems can eliminate the inherent delays associated with round-trip data transmission, which is critical for maintaining safety in autonomous operations. For a high-speed drone navigating a dense urban environment or an industrial sorter identifying defects in milliseconds, the luxury of waiting for a cloud-based response simply does not exist. This shift toward edge inference also addresses growing concerns regarding network bandwidth and data privacy, as sensitive visual information can be processed locally and discarded, leaving only the relevant metadata to be transmitted for further analysis. Consequently, the demand for dedicated edge hardware has skyrocketed, leading to a crowded market of specialized chips designed specifically for low-latency tasks.

In the pursuit of achieving superior performance-per-watt, the vision industry is rapidly moving away from general-purpose graphics cards in favor of custom and semi-custom application-specific integrated circuits. In many power-constrained environments, such as battery-operated medical devices or remote surveillance cameras, traditional processors consume far too much energy and generate excessive heat that can degrade system reliability. Custom silicon allows engineers to optimize for the specific neural network architectures used in modern computer vision, providing a significant boost in efficiency and a lower total cost of ownership over the hardware’s lifecycle. Furthermore, the integration of hardware and software is becoming a primary differentiator for silicon vendors; modern hardware is rarely sold as a standalone component anymore. Instead, it is offered as part of a comprehensive AI software stack that enables manufacturers to bypass complex engineering hurdles and bring their vision-enabled products to market with unprecedented speed.

Key Industries Driving Vision Hardware Adoption

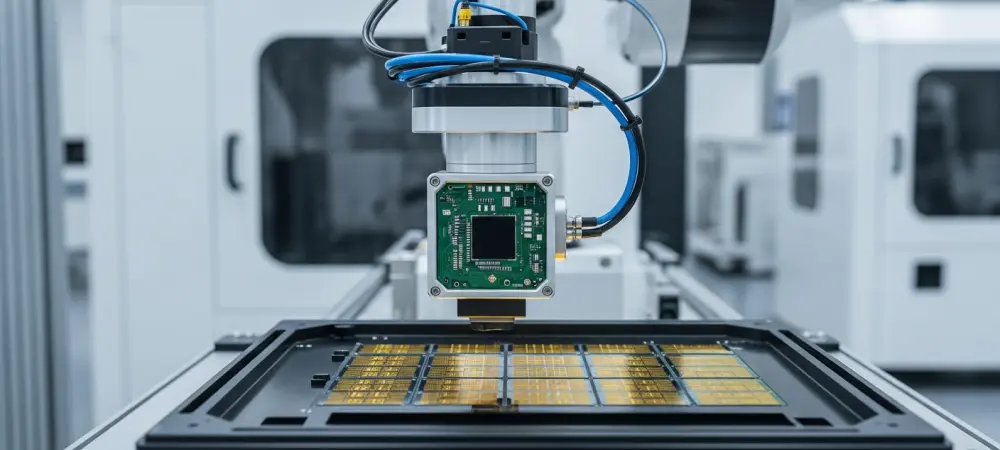

Manufacturing and Semiconductor Excellence: The Industry 4.0 Standard

Industrial automation currently stands as the most significant driver for the vision hardware market, fueled by the aggressive implementation of Industry 4.0 principles across the globe. In modern smart factories, dedicated hardware accelerators allow multi-camera systems to perform incredibly complex tasks such as 3D surface inspection and volumetric measurements in real time without slowing down the production line. As the density of industrial robots continues to increase, the need for accelerators that can identify microscopic anomalies or guide robotic arms with sub-millimeter precision has become a primary growth engine. These systems are moving beyond simple pass-fail checks and are now capable of predictive quality control, where the vision system identifies the early signs of machine wear before a defect even occurs. This level of sophistication requires immense local processing power, further solidifying the necessity of high-performance vision chips in the manufacturing sector.

The semiconductor industry itself has become one of the largest consumers of high-speed vision technology, particularly as fabrication processes move toward increasingly smaller and more complex nodes. Inspecting silicon wafers at the 2-nanometer level involves managing an astronomical amount of visual data, making the use of high-throughput vision accelerators an absolute requirement for modern defect classification and yield management. This specific niche is projected to be among the fastest-growing segments of the market because the complexity of modern electronics leaves no room for human error in quality control. As the demand for more advanced chips for AI and telecommunications grows, the vision hardware used to inspect these chips must evolve in parallel, creating a self-sustaining cycle of innovation. By the time we reach 2035, the integration of AI-driven optical inspection will likely be the only viable method for maintaining the extreme precision required for next-generation semiconductor manufacturing.

Frontiers in Mobility and Healthcare: Redefining Safety and Diagnostics

The automotive and logistics sectors are facing a unique set of challenges that can only be solved through advanced sensor fusion, where data from cameras, radar, and LiDAR are processed simultaneously. These high-growth segments require a multi-accelerator architecture that provides the redundancy and reliability necessary for regulatory approval in autonomous driving applications. The hardware must be capable of identifying objects, predicting pedestrian movement, and reading road signs in all weather conditions, all while operating within the strict thermal and power limits of a vehicle. As e-commerce continues to expand, the deployment of autonomous delivery robots and long-haul trucks will further accelerate the demand for vision chips that can navigate complex, unpredictable environments. This push for mobility is not just about convenience; it is a fundamental shift in how goods and people move, with vision hardware serving as the critical layer of safety and efficiency.

In the medical field, hardware accelerators are fundamentally changing the way clinicians interact with imaging modalities like MRIs, CT scans, and ultrasounds. The focus has transitioned from simply capturing high-resolution images to real-time image reconstruction and AI-assisted diagnostics that help doctors identify life-threatening patterns more accurately and quickly. Furthermore, the development of compact and low-energy vision chips is enabling the rise of point-of-care diagnostic devices, which bring high-quality medical tools to rural and emergency settings where massive imaging equipment is unavailable. These portable devices can perform complex analysis on the spot, allowing for immediate triage and treatment decisions that were previously impossible. By 2035, the ubiquity of these AI-powered medical vision tools will likely have transformed the standard of care, making advanced diagnostics accessible to a much larger portion of the global population.

Competitive Landscapes and Strategic Barriers

Regional Leadership and Market Participants: The New Silicon Geography

The competitive environment for vision hardware is currently a dynamic mix of established semiconductor giants and lean, specialized AI chipmakers aiming to disrupt the status quo. While the traditional leaders still dominate the high-end training markets, emerging players are successfully challenging them with specialized architectures designed specifically for the unique demands of low-latency edge processing. We are also witnessing a trend toward vertical integration, where companies that produce end-user products, such as automotive manufacturers or smartphone giants, are developing their own custom silicon in-house. This allows them to achieve maximum efficiency by tailoring the hardware specifically to their proprietary algorithms, effectively bypassing the limitations of off-the-shelf components. This strategic move creates a more fragmented market but one that is highly optimized for specific use cases, ranging from consumer electronics to heavy industrial machinery.

Geographically, the heart of the vision hardware market remains concentrated in the Asia-Pacific region, which continues to serve as the global hub for both semiconductor production and high-volume consumption. However, North America has maintained its position as a powerhouse for research and development, particularly in the creation of high-reliability applications for the defense and high-end medical sectors. Simultaneously, Europe is carving out a vital role for itself by focusing on the automotive and industrial sectors, where demand is anchored in a long history of safety certifications and strict regulatory compliance. These regional specialties create a complex global supply chain where innovation in one part of the world rapidly influences production in another. As we look toward the next decade, the ability of companies to navigate these regional differences and comply with varying international standards will be a major factor in determining who leads the vision hardware market.

Growth Drivers and Technical Constraints: Navigating the Path to 2035

Several powerful factors are pushing the market forward, including the widespread adoption of AI, rising global labor costs, and an industry-wide commitment to achieving zero-defect manufacturing. As robots and autonomous systems become more economically viable, the vision hardware that powers their “perception” becomes an increasingly essential investment for any organization looking to scale its operations. The availability of pre-validated hardware-software stacks is also a major catalyst, as it allows smaller companies to innovate and deploy sophisticated systems without needing a massive team of silicon engineers. This democratization of vision technology is expanding the market beyond traditional tech sectors into areas like agriculture, retail, and environmental monitoring, where the potential for automation has only recently begun to be realized through the use of intelligent sensors.

Despite the clear path for growth, the industry must still contend with significant hurdles, such as the massive capital requirements for advanced node fabrication and a fragmented global regulatory landscape regarding AI and data privacy. High upfront costs for custom chip design can still be a barrier for many firms, and the lightning-fast pace of technological change means that hardware can face obsolescence in just a few years if it is not designed with flexibility in mind. Successfully navigating these challenges will require a relentless focus on power efficiency and the ability to adapt to a shifting global supply chain that is increasingly influenced by geopolitical considerations. Companies that can bridge the gap between high-performance computing and the practical constraints of the edge will be the ones that thrive as vision hardware becomes the primary interface between the digital and physical worlds.

Strategic Directions for the Next Decade

The transition of vision hardware from a supporting role to a primary architectural component was a defining characteristic of the tech landscape as the decade progressed toward 2035. Decision-makers recognized that the path to success required a departure from general-purpose computing toward a more fragmented, yet highly efficient, silicon landscape. Strategic investments were prioritized in hardware-software co-design to ensure that vision algorithms could run natively on the most efficient gates possible, minimizing both latency and energy consumption. This shift allowed industries to move beyond the limitations of cloud-based processing, enabling a new era of truly autonomous systems that operated with high levels of reliability in the real world. By focusing on these specialized accelerators, organizations managed to overcome the thermal and power bottlenecks that had previously hindered the deployment of sophisticated AI at the edge.

Looking forward, the focus for developers and engineers should shift toward building modular and scalable vision architectures that can adapt to the rapid evolution of neural network models. The industry learned that rigid hardware designs were quickly outpaced by software innovations, making the move toward programmable accelerators like FPGAs and specialized NPUs a critical survival strategy. Furthermore, addressing the ethical and privacy concerns surrounding ubiquitous vision systems remained a top priority, with hardware-level encryption and metadata-only processing becoming the standard for any public-facing technology. As the global economy continues to integrate these intelligent sensors, the ability to maintain a balance between high-performance perception and strict data security will define the next generation of vision hardware. Future developments should prioritize the creation of open standards and interoperable platforms to prevent vendor lock-in and foster a more collaborative ecosystem for vision innovation.