Dominic Jainy brings a sophisticated lens to the intersection of massive hardware logistics and financial sustainability. With a deep background in artificial intelligence and blockchain, he has observed how tech giants leverage their capital to dictate global market terms. In this discussion, he unpacks the recent surge in mobile DRAM procurement, examining how a consumption of 2.4 exabytes of memory shapes the global supply landscape and why service-oriented revenue streams are becoming the ultimate shield against manufacturing volatility.

Apple is reportedly securing vast quantities of mobile DRAM, potentially sidelining competitors from their shipment targets. How does this aggressive procurement strategy impact long-term supplier relationships, and what specific operational steps can smaller manufacturers take to protect their supply chains?

When a giant moves to vacuum up all available mobile DRAM, it sends a shockwave through the entire semiconductor ecosystem that suppliers both love and fear. These suppliers find themselves in a lucrative but dangerous bind, feeling the thrill of fulfilling a 240-million-unit order while worrying about the long-term risk of becoming a captive vendor to a single master. For smaller manufacturers, the scent of desperation is real as they watch their allocation vanish into the hands of a dominant player, often leaving them with no choice but to pay a premium for whatever is left. To survive, these smaller entities must pivot toward “just-in-case” inventory models or seek long-term, legally binding contracts that guarantee a minimum floor of supply even during these aggressive hoarding phases.

While hardware components like memory fluctuate in price, service-based revenues from cloud storage and digital subscriptions are often cited as a hedge. Can you explain how these high-margin services balance out volatile production costs, and what specific metrics indicate a successful transition to this revenue model?

The transition from a pure hardware vendor to a service-heavy ecosystem is the holy grail of financial stability in the modern tech world. High-margin offerings like iCloud+, AppleCare+, and advertisement revenue in the App Store act as a powerful cushion against the “melee” of fluctuating component costs. When the price of LPDDR5 spikes due to scarcity, the recurring revenue from a digital subscription doesn’t flinch, maintaining a steady flow of cash that keeps overall corporate margins healthy. Analysts look for specific indicators of success here, such as the attach rate of services per device sold and the sustained growth in advertisement-related revenues across platforms like Apple Maps.

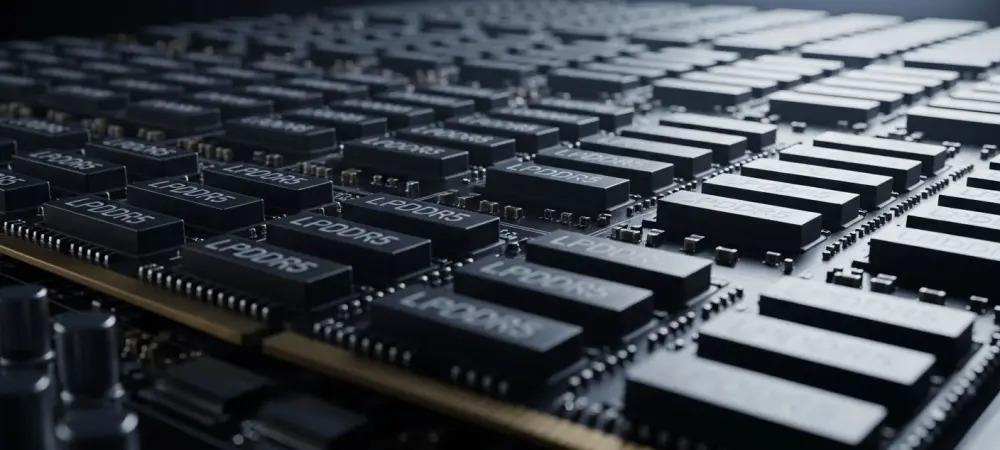

Consuming 2.4 exabytes of LPDDR5 memory for a single smartphone lineup represents a massive logistical undertaking. What are the primary technical challenges of managing this volume of high-speed memory, and how do shipment targets of 240 million units influence the global pricing index for mobile components?

Coordinating the movement of 2.4 exabytes of LPDDR5 is a feat of engineering and logistics that few companies on earth could even attempt without catastrophic failure. Technically, ensuring the quality and consistency of such high-speed memory across 240 million units requires a rigorous, multi-layered testing protocol to prevent mass recalls that could cost billions. When one entity sets such a massive shipment target, it effectively resets the global pricing index, as the scarcity of the remaining supply drives costs through the roof for everyone else. This creates a high-pressure environment where the sheer gravity of one company’s demand pulls the entire market’s pricing toward a breaking point for smaller competitors.

If a single tech giant dominates the available supply of mobile memory, it forces rivals to adjust their product roadmaps. What are the immediate trade-offs for competitors facing chip shortages, and what strategic pivots should they implement to remain viable when key hardware components are being hoarded?

Competitors facing a shortage of critical components are often forced into painful trade-offs, such as downgrading the specs of their flagship devices or delaying launch dates until the supply chain stabilizes. Watching a rival hoard memory can feel like being squeezed out of a room, leaving others to scramble for leftover chips that may not meet the performance standards of modern consumers. To remain viable, these companies must double down on software optimization, making their existing memory go further through clever engineering, or diversify their roadmaps to include mid-range devices that don’t rely on the same high-tier LPDDR5 chips. This strategic pivot allows them to maintain a market presence while waiting for the procurement storm to pass.

What is your forecast for the mobile DRAM market?

I anticipate that the mobile DRAM market will enter a period of extreme polarization where the top-tier supply is almost entirely spoken for by the industry’s largest players months in advance. As demand for AI-driven features in smartphones increases the need for high-speed memory, the 2.4 exabyte appetite we see today will likely become the new baseline rather than a one-time anomaly. We will see a shift where memory becomes the most critical bottleneck in device performance, leading to a two-tier market of “memory-rich” and “memory-poor” consumer electronics. This will force a new era of transparency in supply chains, as investors demand more visibility into who actually holds the physical chips in an increasingly scarce environment.