AI-driven data centers are scaling so fast that grid operators, local planners, and corporate buyers are colliding over timing, reliability, and siting as the race accelerates to pair fast-to-build solar with storage so 24/7 compute does not outstrip the power system that keeps it alive. The result is a rapid shift from pure renewables enthusiasm to a more pragmatic, hybrid toolkit.

The surge matters because large data centers are among the biggest new loads on U.S. grids and their procurement choices ripple into reliability, emissions, and siting. In this landscape, Virginia serves as a bellwether, with national lessons for developers and buyers.

Market Reality: Demand Growth and Early Deployments

Quantifying the Surge: Load Growth, Grid Warnings, and Adoption Trends

Virginia’s latest outlook projected electricity consumption could triple by 2040, a stark proxy for hot spots where AI and high-density compute concentrate. That trajectory reframed siting from a land-use debate into a system adequacy question.

PJM flagged potential shortfalls under extreme summer conditions, underscoring how demand is sprinting ahead of firm capacity. The state’s imports exceeded 50 million MWh in 2023, signaling a structural gap between load and local generation.

Even with policy ambiguity, corporate clean energy buying is accelerating, and solar remains the fastest-to-market new build in many regions. That speed is now central to portfolio hedging, especially as wholesale volatility rises.

Real-world Applications: Data Center Hubs, Fast Permitting, and Early Storage Pairings

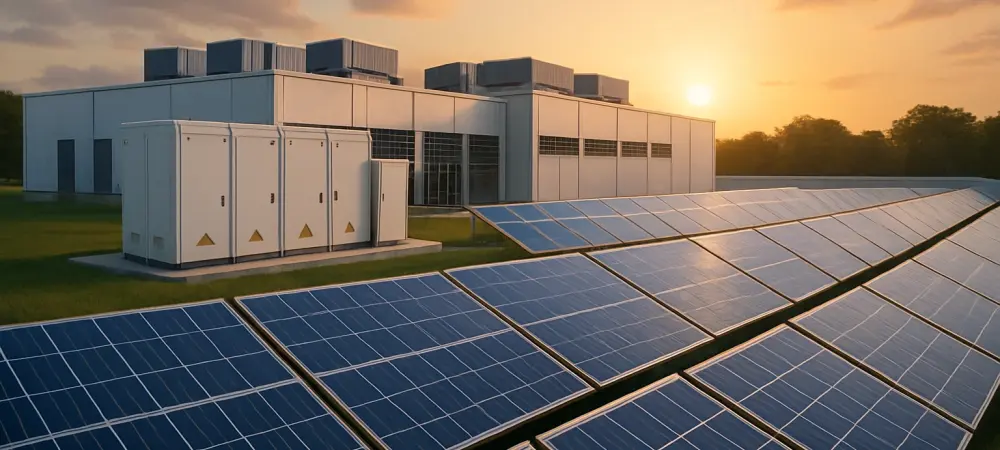

Virginia’s Permit By Rule pathway for projects up to 150 MW can move from application to operation in roughly two years. Behind-the-meter arrays are even quicker, often measured in months rather than years. Co-location is moving from pilot to playbook. Google partnered with Intersect Power on hybrid sites and already operates 312 MW of batteries, proving that storage adds practical firmness to solar-heavy portfolios.

Corporate portfolios scaled quickly. Microsoft added more than 860 MW of solar in 2024, Meta is building 900+ MW in Texas, and Amazon leads with 13.6 GW underway, including a 500 MW Webb County project and over 20 Texas builds.

Expert Insights and Stakeholder Perspectives

Janta Power’s CEO argued that market demand, efficiency, and scalability will keep pulling solar into data center portfolios. In his view, these buyers could become first adopters of advanced solar that later diffuses across the market. JLL’s data center advisors cautioned that behind-the-meter solar alone is insufficient for large, high-density sites due to intermittency and space constraints. Their guidance: treat solar as one pillar in a diversified energy stack. Grid operator voices, including PJM, noted that the demand ramp is outpacing firm additions and interconnection progress. Reliability planning now hinges on both the magnitude of load and the speed of bringing new capacity online.

Solar’s Promise—and Its Limits—for 24/7 Compute

Why Solar Keeps Winning: Speed, Cost, and Policy Pathways

Speed-to-market is decisive. Sub-150 MW permitting and modular onsite arrays compress timelines when loads cannot wait for long-cycle generation.

Costs and hedging benefits reinforce the case, with competitive LCOE and protection against price spikes. As a grid resource, solar displaces fossil units and relieves peak stress.

Physics and Footprint: The Barriers to “solar-only” Data Centers

Capacity factor realities—near 22% in many markets—constrain round-the-clock coverage without firming. Batteries offset that gap, but only for limited durations today.

Land intensity also bites. A 200 MW data center could require 1,000+ acres of conventional panels, a scale that triggers siting friction and grid interconnection hurdles.

Corporate Procurement is Rewriting the Deployment Map

Who’s Buying and Where: Big Tech’s Scale and Spread

Amazon’s 13.6 GW pipeline spans more than 20 Texas projects and a 500 MW Webb County farm. That scale sets local market tempo and interconnection priorities. Microsoft added 860+ MW of solar in 2024 and grew a clean energy portfolio exceeding 34 GW. Meta’s three Texas projects totaling 900+ MW anchor a hub strategy. Google’s 312 MW of batteries and co-location with Intersect Power signal a pivot to hybridization. Storage duration is creeping upward to match evening peaks.

Strategies Evolve: From Ppas to Hybrids and Co-location

Procurement is shifting from single-source PPAs to solar-plus-storage with longer durations for peak coverage. Co-optimization beats pure energy-only buys.

Geographic diversification smooths intermittency and matches load across regions. Some buyers now fund interconnection upgrades to pull projects forward and stabilize supply.

Siting Friction and Policy Uncertainty

Local Opposition and the Shift to Smaller, Faster Projects

Counties in Virginia rejected more solar megawatts in 2024 than they approved, reflecting concerns about land use, viewsheds, and rural industrialization. Timelines stretched as hearings multiplied. Developers responded by favoring smaller, distributed sites in friendlier jurisdictions to keep schedules intact. Incremental megawatts became a strategy rather than a compromise.

Federal Signals: Approvals, Reviews, and the Risk of Delay

The canceled environmental review for Esmeralda 7 cast a chill over marquee proposals, even as corporate demand grew. Financing models adjusted to policy whiplash risk. The implication was clear: long-lead projects faced more uncertainty, increasing the value of flexible, phased builds and standardized hybrid blocks that can scale.

Hybrid Pathways That Work Now

Solar-plus-storage Architectures for Data Centers

Two-to-four-hour batteries handle peak shaving, ramp coverage, and short outages, firming solar output without chasing full 24/7 replacement. Longer cycles are emerging but remain niche.

Value stacking supports the economics: energy arbitrage, demand charge reduction, and ancillary services add revenue and resilience while reducing grid stress.

Grid-integrated Models: Co-location, Microgrids, and Interconnection Upgrades

Co-location offers shared interconnections and better production profiles, trimming capex per delivered megawatt. The grid sees smoother injections and fewer curtailments. Microgrids blend onsite solar, batteries, and backup generation to meet strict SLAs. Some buyers co-fund network upgrades to shrink queues and lock in reliability.

Metrics and Decision Framework for Operators

Sizing and Siting Checklist

Operators map 24/7 load profiles, peaks, and N+1/N+2 resilience targets to right-size assets. Land availability and queue position shape what is feasible, where, and when.

Storage duration and cycling strategy separate cost savings from resilience. Two-to-four-hour systems dominate today, with selective pilots probing longer durations.

Procurement and Portfolio Design Checklist

Contract mixes across physical and virtual PPAs, tolling, and hedges spread risk. Hybridization and co-location options align deliveries with compute ramps.

Community engagement and permit risk move to the front of the playbook. Benefits agreements and transparent siting criteria shorten cycles and stabilize outcomes.

Conclusion: Solar’s Growing Role—inside a Diversified, Storage-backed Strategy

Demand growth outpaced firm capacity, yet solar’s speed and cost kept it central while storage firmed its value. Corporate buyers shaped build locations, timelines, and interconnection priorities through hybrid procurement and co-location. The practical next steps were clear: scale standardized solar-plus-storage blocks, invest in targeted grid upgrades, and design portfolios that blend onsite resilience with regional balancing. By doing so, operators unlocked reliable power for 24/7 compute, reduced exposure to volatility, and advanced decarbonization without betting on any single technology.