Unveiling a Critical Challenge in Auto Lending

In the current landscape of auto lending, a staggering 3.3% of all loan applications in the first half of this year were flagged as fraudulent, with a sharp spike to 5.5% in May alone, according to industry data. This alarming statistic underscores a pervasive issue: identity theft has become a primary engine fueling auto loan fraud, outpacing fraud rates in other financial sectors like credit cards, which stand at just 2.7%. The auto lending market, involving high-value transactions and multiple stakeholders, presents unique vulnerabilities that criminals exploit with increasing sophistication. This market analysis aims to dissect the trends, vulnerabilities, and future projections surrounding this escalating crisis, offering critical insights for lenders, dealerships, and policymakers striving to safeguard the industry.

Dissecting Market Trends: The Surge of Identity Theft in Auto Lending

Current Landscape: Fraud Rates and Key Statistics

The auto lending sector is grappling with an unprecedented wave of fraud driven by identity theft. Unlike synthetic fraud, which involves completely fabricated identities and accounts for only 0.8% of cases, identity theft dominates as the primary method, leveraging stolen personal data to bypass verification processes. This trend is particularly pronounced due to the high monetary value of auto loans, often ranging into tens of thousands of dollars per transaction. The discrepancy between fraud detection in auto loans and other financial products highlights a critical gap in security measures, positioning this market as a prime target for criminal activity.

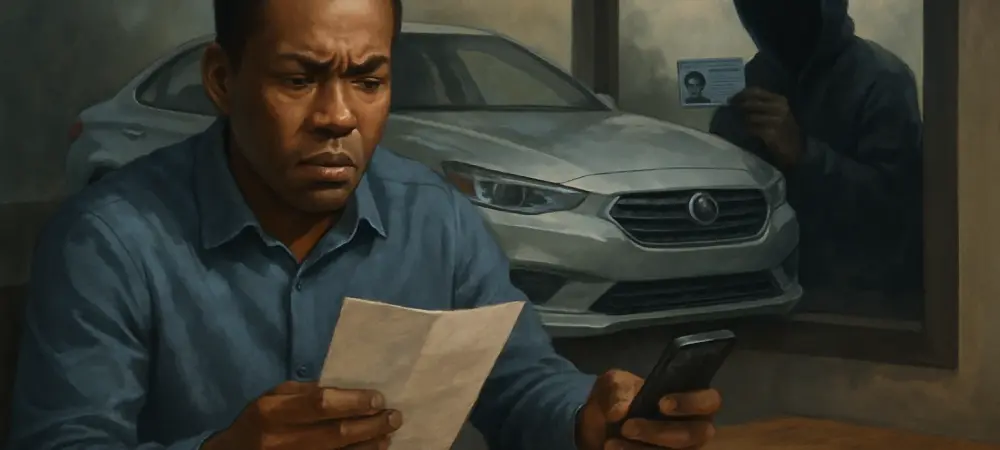

Vulnerable Touchpoints: Where the System Falters

A deeper look into the auto lending ecosystem reveals systemic weaknesses that facilitate fraudulent activities. The process often involves multiple parties—buyers, dealerships, and lenders—creating numerous opportunities for deception. Manual identity verification, still prevalent at many dealerships, lacks the speed and accuracy of digital systems used in other sectors, allowing fraudsters to secure loan approvals before thorough checks are conducted. This fragmented approach contrasts sharply with real-time fraud detection algorithms employed in credit card markets, exposing auto lenders to significant financial risks.

Criminal Ingenuity: Evolving Tactics in Fraud Schemes

Fraudsters have adapted to exploit these vulnerabilities with highly coordinated schemes. In a notable case from Miami, authorities dismantled a complex fraud ring that utilized stolen identities to acquire luxury vehicles, involving complicit dealership staff and manipulated vehicle titles through corrupt channels. These vehicles were either exported or disguised through rental business fronts, illustrating the multi-layered strategies employed. Such operations often include fabricating credible credit histories using stolen data, further complicating detection efforts and amplifying losses for lenders.

Future Projections: Navigating Emerging Risks and Solutions

Anticipated Trends: Dominance of Identity Theft over Synthetic Fraud

Looking ahead, identity theft is expected to remain the predominant form of fraud in auto lending, largely due to the practical challenges of using fully synthetic identities in a process that frequently requires physical presence and documentation. Projections suggest that without significant advancements in fraud prevention, losses could escalate, potentially impacting market stability. The reliance on outdated verification methods continues to hinder the industry’s ability to counter sophisticated criminal tactics effectively.

Technological Horizons: Innovations to Bridge Security Gaps

Emerging technologies offer a glimmer of hope for mitigating these risks. AI-driven identity verification systems and real-time data analytics are poised to revolutionize fraud detection by identifying discrepancies at the point of application. However, adoption remains inconsistent across the market, with smaller dealerships and lenders lagging behind due to cost constraints. If widely implemented, these tools could significantly reduce fraud rates, providing a much-needed shield against identity theft-driven schemes.

Regulatory Outlook: Shaping a More Secure Market

Regulatory developments are also on the horizon, with discussions around mandating stricter digital verification standards gaining traction. Such measures could standardize security protocols across the industry, reducing the variability in fraud prevention capabilities between large and small players. Over the next few years, from this year to 2027, potential policy shifts may compel lenders to invest in modern systems, addressing long-standing vulnerabilities and fostering a more resilient auto lending environment.

Reflecting on the Path Forward: Strategic Imperatives

This analysis uncovers the profound impact of identity theft on auto loan fraud, with data revealing a troubling rise in fraudulent applications that outstrips other financial sectors. Systemic gaps, coupled with sophisticated criminal strategies, expose the fragility of current practices in the auto lending market. Moving forward, stakeholders must adapt by prioritizing investments in real-time verification technologies and advocating for uniform regulatory standards to fortify defenses. Comprehensive training for dealership staff emerges as a vital step to enhance fraud detection at critical touchpoints. Ultimately, collaborative efforts between lenders, policymakers, and technology providers will lay the groundwork for a more secure future, ensuring that the industry can navigate evolving threats with greater confidence.