The End of the Cash-Only Commute in South Africa

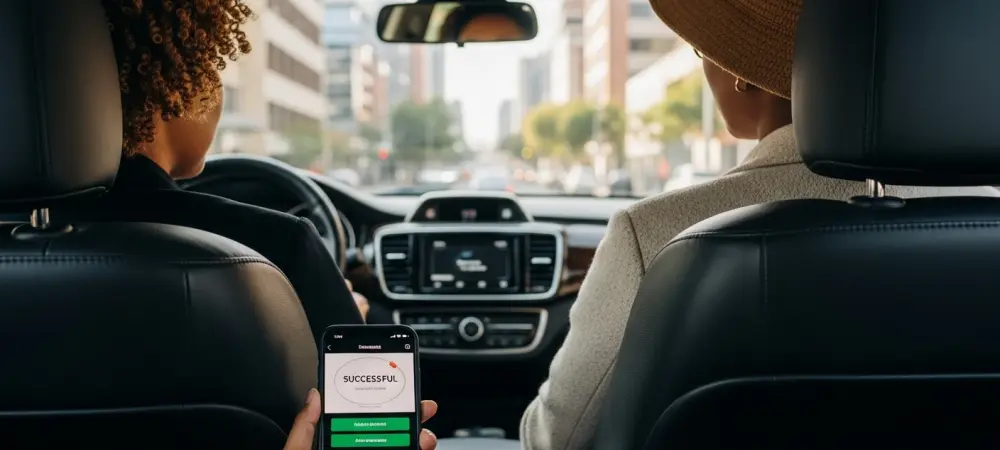

The rhythmic exchange of paper bank notes in South African minibuses and private cars is gradually fading as digital wallets begin to dictate the pace of modern urban mobility. As passengers and drivers seek safer, more efficient ways to navigate bustling urban centers, the partnership between cross-border payment powerhouse dLocal and global mobility giant inDrive arrived to bridge the gap between physical movement and digital finance. This collaboration was not just about adding a button to an app; it represented a fundamental re-engineering of how money flows through the streets of Johannesburg, Cape Town, and beyond.

South Africa’s transit landscape is undergoing a silent revolution where the jingle of loose change is being replaced by the seamless notification of a digital transaction. By integrating modern fintech into the everyday ride-hailing experience, the two companies moved toward a model that prioritizes user convenience. This shift acknowledged the necessity of modernizing the transport sector to meet the demands of a tech-savvy population while maintaining the essential reliability required for daily commuting.

Bridging the Digital Divide in Emerging Mobility Markets

The South African transport sector has long grappled with the dual challenges of financial exclusion and physical security. For years, the heavy reliance on cash made both drivers and passengers targets for theft, while simultaneously slowing down the speed of commerce. This new initiative addressed these systemic issues by integrating modern fintech into the everyday ride-hailing experience.

By moving toward a digital ecosystem, the partnership aligned with a global shift toward hybrid financial models. These systems offer the sophistication of digital payments while respecting the economic realities of markets where cash remains a vital, albeit risky, tool. This balance ensured that no segment of the population was left behind during the transition to a more digital economy.

The “One dLocal” Framework: A Unified Financial Engine

At the heart of this launch is a sophisticated end-to-end financial model powered by a single API integration. At the heart of this launch is a sophisticated end-to-end financial model powered by a single API integration. This technical milestone allowed for a multi-faceted approach to money movement that was previously fragmented. The system handles local credit and debit card acceptance for passengers, ensuring that booking a ride is as simple as a tap on a smartphone screen. Simultaneously, the framework manages real-time fare splitting and domestic payouts, ensuring that drivers are not left waiting days for their earnings. By utilizing dLocal’s localized payment rails, inDrive bypassed the traditional hurdles of cross-border banking, keeping the capital flowing within the domestic economy. This efficiency significantly reduced the administrative burden on the platform while increasing trust among its workforce.

Industry Perspectives on Security and Scalability

Leadership from both organizations viewed this South African launch as a proof-of-concept for broader global ambitions. Ashif Black of inDrive emphasized that driver satisfaction is directly tied to the reliability and speed of payouts, noting that financial trust is the backbone of the mobility industry. Without a secure method for receiving funds, the growth of any mobility platform remains inherently limited by human hesitation.

Meanwhile, Barrie Swart of dLocal pointed to this partnership as a scalable blueprint. With dLocal already operating in over 44 markets, this unified model was designed to be exported to other regions across Africa, the Middle East, and Latin America. This allowed global companies to manage complex local payments without establishing dozens of different regional entities, effectively streamlining international expansion.

Navigating the Transition to a Cashless Ecosystem

For businesses looking to replicate this success, the partnership provided a clear framework for digital transition. The strategy prioritized safety by reducing the “cash on hand” risk, which lowered the likelihood of fraud and roadside theft. However, it also maintained an inclusive “cash-optional” feature, acknowledging that total digitization cannot happen overnight in a diverse economy.

The initiative effectively demonstrated how technical integration could be harmonized with cultural nuances. Stakeholders observed that providing rapid liquidity to drivers while securing passenger data created a more resilient environment for future investment. The transition proved that local card acceptance and a single point of technical integration were the primary drivers for sustainable growth in emerging markets. This successful deployment paved the way for more integrated financial services across the continent.