A seemingly innocuous set of open-source text files from a small startup recently triggered a stock market disruption of unprecedented scale, wiping out a staggering $285 billion in market capitalization from established software-as-a-service (SaaS) giants. This event, now dubbed the “SaaSpocalypse,” was more than just a momentary panic; it was a powerful market signal that the ground beneath the enterprise software landscape is fundamentally shifting. The ensuing competition between established behemoths like Microsoft, with its Copilot platform, and nimble disruptors like Anthropic, with its nascent Cowork tool, has become a high-stakes battle for the very future of knowledge work. This is not merely a race to build a better product but a clash of philosophies over the foundational architecture of enterprise AI. This analysis will dissect the architectural, strategic, and philosophical differences between these competing approaches to reveal the critical trends shaping enterprise AI adoption and the future of workplace productivity.

The Emerging AI Divide Vision vs Reality

Market Disruption and Adoption Metrics

The “SaaSpocalypse” provided a dramatic and quantifiable measure of the market’s anxiety. The $285 billion loss in value across the SaaS sector underscored a growing belief among investors that a new, simpler architectural layer could render many existing application-based platforms obsolete. This disruption occurred against a backdrop of challenging enterprise AI adoption metrics. Reports over the past year have consistently highlighted a significant gap between the hype surrounding platforms like Microsoft Copilot and the reality of their deployment. Many organizations have balked at the high per-user costs, struggling to build a convincing ROI case for multi-million dollar annual contracts.

These cost concerns are compounded by profound technical and organizational complexities. The rollout of Copilot often requires extensive and costly data governance audits to untangle years of poorly configured permissions in systems like SharePoint, creating a significant barrier to entry. In stark contrast, the rapid, organic growth of Anthropic’s initial tools points toward a powerful counter-trend: the bottom-up, developer-first adoption model. This strategy, where individual users or teams adopt a tool for its immediate utility, bypasses the lengthy top-down procurement cycle and builds a groundswell of internal support, proving that value, not a sales pitch, is the most effective go-to-market strategy.

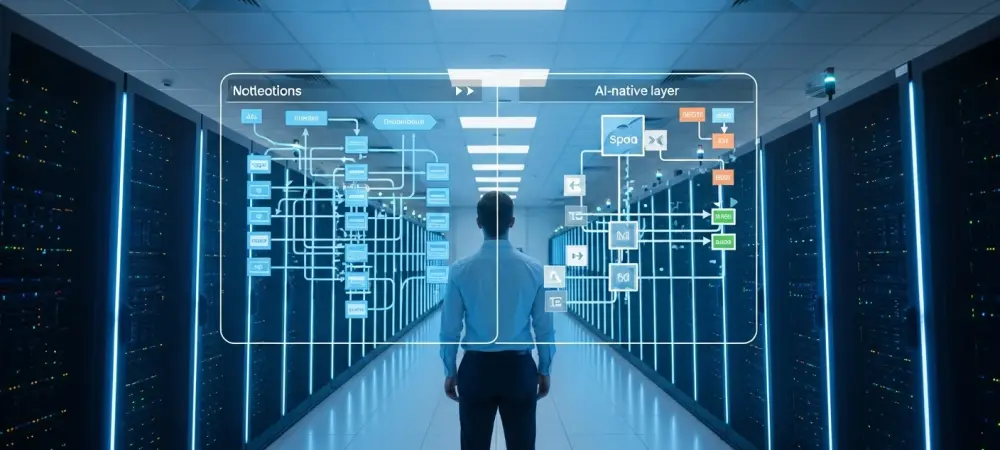

A Tale of Two Architectures Copilot and Cowork

The divergent market responses can be traced directly to the fundamentally different architectural philosophies of the two platforms. Microsoft Copilot is an application-centric model, deeply woven into the fabric of its existing Microsoft 365 ecosystem. It functions as an intelligent feature embedded within the sidebars of Word, Excel, Teams, and Outlook. Its power and context are derived from the Microsoft Graph, an immensely complex and powerful but notoriously difficult-to-manage API for an organization’s data. This design choice structurally limits Copilot to operating within the silos of these applications, enhancing existing workflows rather than creating a new, universal way of working.

In sharp contrast, Anthropic’s Cowork represents a radically simpler, file-system-native approach. It presents the user with a single, universal text box that operates directly on the files stored locally on their machine. It is not a feature within an application; it is an organizing layer that sits below all applications. This architecture allows it to read, create, and modify any file type—be it a document, spreadsheet, or presentation—without being tethered to a specific software suite. The accessibility of this model is best exemplified by its plugin system; instead of requiring a complex low-code development platform, new capabilities can be added by creating simple markdown files, effectively democratizing the creation of custom AI agents for any user who can write a clear sentence.

Strategic Analysis The Innovator’s Dilemma in the AI Era

Microsoft’s approach to enterprise AI can be clearly viewed through the lens of the classic innovator’s dilemma. As a dominant incumbent, its primary strategic imperative was to protect its massive enterprise licensing model, its vast suite of existing products, and its extensive partner ecosystem. This structural burden meant that every decision about Copilot had to accommodate legacy systems and business models. The need to integrate AI into existing applications prevented Microsoft from building a truly independent and universal organizing layer. The result was a fragmented and complex product ecosystem, bound by the constraints of seats, licenses, and administrative controls designed for a pre-AI era.

Anthropic, on the other hand, enjoyed an unconstrained advantage as a disruptor with no legacy business to defend. This freedom allowed its developers to approach the problem from first principles, focusing singularly on solving the user’s core challenge: how to get work done more efficiently. Without the need to accommodate existing infrastructure or protect established revenue streams, they could design a more fundamental product. By operating at the file system level, Cowork bypasses the application layer entirely, delivering a solution that is architecturally purer and more directly aligned with the user’s intent.

This strategic divergence is mirrored in the companies’ go-to-market strategies. Microsoft employed its traditional top-down enterprise sales motion, targeting CIOs and IT departments with large-scale, multi-year contracts. This approach has met with significant friction, as leaders question the high cost and unclear returns. In contrast, Anthropic’s success follows a modern, bottom-up paradigm that has proven successful for other transformative platforms like AWS, GitHub, and Slack. It began with a specialized tool for developers that gained organic traction before being adapted for a broader audience of knowledge workers. This model, where individual adoption and proven value precede corporate procurement, represents a significant shift in how enterprise software is bought and sold.

Future Outlook The Triumph of Simplicity

The battle between these two models suggests the emergence of a new, foundational architectural layer for knowledge work. Simple, file-system-native AI agents have the potential to become the next universal interface, abstracting away the application-based SaaS model that has dominated the last decade. Users may no longer need to open a half-dozen different programs to complete a complex task; instead, they could simply issue a natural language command to an agent that orchestrates the work across all relevant files and systems. This represents a profound disruption to the current software landscape.

However, both approaches face significant hurdles. Copilot’s primary challenge is overcoming the immense friction created by its cost, complexity, and data governance requirements. It must prove its value proposition is compelling enough to justify the organizational overhaul needed for its successful deployment. Conversely, Cowork’s challenge is one of maturation. As a research preview, it currently lacks the enterprise-grade security, compliance, and governance features that large organizations demand. Its path to success lies in scaling to meet these requirements without sacrificing the radical simplicity that makes it so compelling.

The broader implication for enterprise IT is that the most transformative AI tools may not arrive through traditional vendors or established procurement channels. The current trend indicates a future where user experience and the elegant removal of friction will triumph over feature-rich but complex ecosystems. The market is signaling a clear preference for tools that are intuitive, accessible, and deliver immediate value, rather than platforms that require extensive training and administrative overhead.

Conclusion Redefining the Enterprise AI Playbook

The trajectory of enterprise AI revealed a clear narrative: while Microsoft brilliantly articulated the vision for an AI-powered future of work, its execution was constrained by the weight of its own success. Its inherent complexity created an opening for a smaller, more agile competitor to deliver a more functional and elegant version of that same vision, not by design, but through a relentless focus on simplicity. This dynamic confirmed that the market’s appetite for functional, intuitive, and accessible AI tools far outweighed its loyalty to established, all-encompassing enterprise suites.

Ultimately, the most resonant trend was the shift in value from feature density to user-centricity. The future of productivity was not defined by the company that could build the most features, but by the one that could most effectively remove the friction between a user’s intent and a completed task. This forced a critical re-evaluation for enterprise leaders, who were urged to look beyond their established vendors and procurement processes. The “SaaSpocalypse” was not just a financial event; it was a clear signal that the playbook for enterprise software was being rewritten, with simplicity as its guiding principle.