A Split-Second Test Before Money Moves

Every instant payment promises certainty in seconds, yet that very speed invites deception to sprint through the cracks unless a smarter check happens before the funds are gone for good. The Federal Reserve Financial Services is moving that check to the front of the line with a network intelligence API that scores risk as a payment is initiated, not after it lands.

The pitch is simple but urgent: keep instant intact while making misdirection harder. Rather than slowing transfers, the service offers real-time signals to help institutions decide whether to proceed, hold, or review. It amounts to a new kind of perimeter—one that learns from behavior seen across the FedNow network and adapts as fraud patterns shift.

Why the Stakes Rose With Instant Everything

FedNow now hums nonstop over FedLine, extending immediate funds availability across more than 9,000 institutions directly or through agents. Convenience has become table stakes, and reliability sits alongside it. That combination changed how customers behave—and how criminals plot. Authorized push-payment fraud forced a rethink. Once a customer is tricked into sending money, recovery becomes a race that many banks lose. Traditional, after-the-fact controls struggle here, because the “authorization” looks legitimate. Network-level context offers a way to challenge that surface logic without punishing good customers.

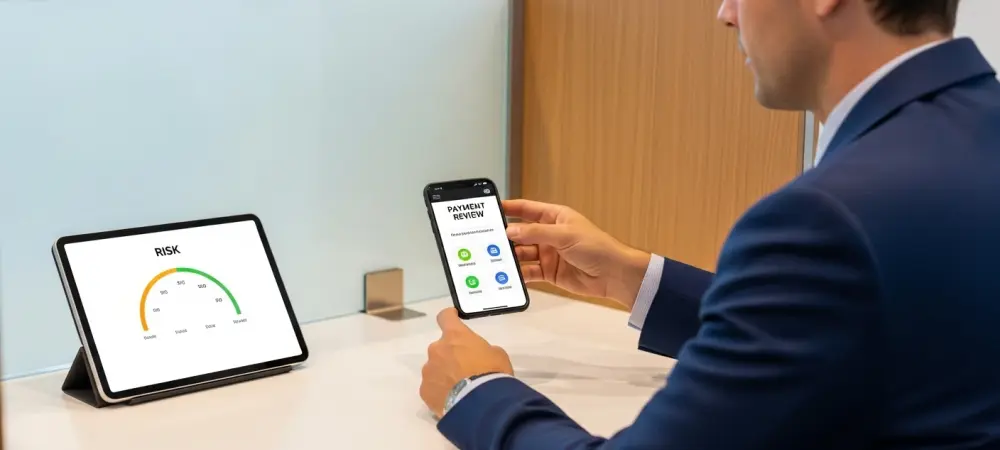

Inside the New Brain: Signals, Context, and Fit

Since April 28, early adopters have been tapping pre-payment signals that surface the moment a sender initiates a transfer. The API synthesizes receiver account-level patterns across the FedNow network with each participant’s internal data, generating a sender-side risk view before execution. “Integration was straightforward, and the value was immediate,” one early adopter’s program lead said.

Institutions can use those scores to nudge customers when risk is elevated. A simple prompt—“This payee looks unusual for you”—can interrupt a coerced payment without blocking legitimate flows. Planned additions sharpen the edge: real-time Payee Name Verification via FedDetect would cross-check names and account details, and alignment with the FraudClassifier model keeps internal analytics consistent and auditable.

Crucially, the service is built to fit instant rails. The decisioning happens fast enough to preserve immediate availability, supporting consistent policies even when processors, cores, and service providers differ. “Cross-network behavior lights up anomalies we never saw in our own walls,” an operations executive noted.

From Proving Ground to Playbook

Early testers describe patterns that feel obvious in hindsight but were invisible locally: first-use accounts receiving high-velocity inflows, tightly timed bursts from newly created profiles, or repeat recipients spanning multiple institutions. “Those cases used to pass one-by-one; the network view stitched the puzzle together,” a fraud strategist said. The operational story runs in parallel. Banks are defining thresholds—proceed, hold, review—and wiring feedback loops so model outcomes retrain quickly. Some are piloting by corridor, segment, or use case while measuring interception rates, false positives, time-to-decision, and abandonment. Others are drafting 24/7 escalation playbooks so risky transactions do not stall beyond service-level promises.

Customer experience sits in the balance. Over-alerting erodes trust; silence invites loss. Institutions report that targeted prompts, paired with streamlined recovery paths and clear education on APP scams, reduce regret without adding friction. Name verification in markets like the UK cut misdirected payments materially, and practitioners expect a similar lift when real-time checks arrive here.

What It Meant for Instant Rail Confidence

By moving intelligence to the moment of initiation, the network shifted the fight toward prevention rather than recovery. Institutions gained a new signal layer, customers encountered smarter prompts instead of hard stops, and fraud teams saw cleaner taxonomy for root-cause analysis. The practical next steps were clear: embed pre-payment decisioning, pair network signals with name verification as it activates, and standardize labeling to learn faster. Speed stayed nonnegotiable, but safety stopped trailing it—an overdue correction that set the tone for instant payments going forward.