Securing a loan for a new sofa or splitting a dinner bill with friends no longer requires a separate trip to a banking app; these financial actions now happen seamlessly within the retail and social platforms people use every day. This fundamental shift marks the rise of embedded finance, where banking services are woven directly into the fabric of non-financial digital experiences. The old model of finance as a distinct destination is giving way to a new paradigm of integrated, contextual services. This analysis will dissect the key drivers fueling this boom, explore parallel fintech trends accelerating its growth, examine the future opportunities and challenges on the horizon, and offer a concluding perspective on this transformative integration.

The Mechanics and Momentum of Embedded Finance

Charting the Explosive Growth Curve

The embedded finance sector is not just growing; it is expanding at an exponential rate, with market projections indicating a multi-trillion-dollar valuation by the end of the decade. This rapid ascent is fueled by consumer demand for convenience and the strategic imperative for brands to offer more integrated services.

Industry leaders predict this trend will “explode,” pushing financial transactions far beyond traditional e-commerce checkouts. The next frontier includes social media platforms, in-car applications, and other daily-use digital environments becoming primary venues for consumer financial activities. This evolution suggests a future where finance is an invisible, yet indispensable, layer of our digital lives.

Real-World Applications and Strategic Benefits

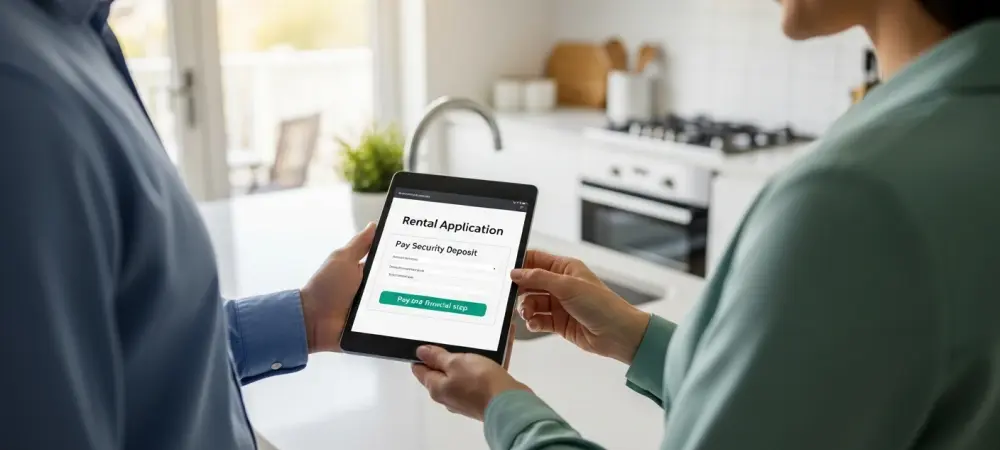

Concrete examples of embedded finance are already widespread, from “buy now, pay later” (BNPL) options integrated into retail apps to point-of-sale lending offered directly on a home contractor’s service platform. These tools remove friction from the customer journey, making it easier for consumers to access credit and complete purchases at the moment of intent. The core strategic advantage lies in meeting customers where they are already active, creating a powerful “mutual stickiness.” This synergy strengthens customer loyalty by providing a seamless experience, benefiting the brand, the digital platform, and the financial provider simultaneously. In this model, a single smooth transaction can secure a customer for all three entities.

Expert Insights on Key Industry Catalysts

The Regulatory Pathway Fintechs Seeking Bank Charters

A key catalyst for the embedded finance surge is an evolving regulatory landscape that has become more receptive to innovation. In response, a growing number of fintech companies are expected to pursue full bank charters, allowing them to operate more independently and expand their service offerings without relying solely on partner banks.

However, this path is not a universal solution for every fintech. Executives caution that seeking a bank charter is not a “one-size-fits-all” strategy. The process remains a significant and complex undertaking, and regulatory approval is by no means guaranteed, requiring substantial investment and a robust compliance framework.

The Automation Wave Agentic Finance for Consumers

Parallel to the growth of embedded services is the expansion of “agentic finance,” where automated, AI-driven guidance for personal finance becomes a mainstream consumer tool. This trend moves beyond simple transaction alerts to offer proactive, personalized financial management directly within embedded experiences.

Practical applications include AI-powered tools that automatically identify and suggest moves to high-yield savings accounts or intelligently schedule credit card payments to optimize rewards and minimize interest. These automated agents enhance the value of embedded finance, making financial wellness more accessible and effortless for the average user.

The Future Landscape Opportunities and Obstacles

Digital Assets Promise Tempered by Practicality

Looking ahead, the growing tokenization of financial assets represents a significant area of innovation that could intersect with embedded finance. The ability to represent traditional assets like real estate or securities as digital tokens on a blockchain promises to increase liquidity and accessibility.

In contrast, broad consumer adoption of more volatile digital assets like stablecoins and cryptocurrencies is expected to remain slow. Experts suggest this hesitation stems from a lack of clear, compelling use cases for the average consumer, who currently sees little practical advantage over traditional payment and investment systems.

Overcoming User Friction in a Decentralized World

The primary obstacle hindering wider adoption of decentralized digital assets is a fundamentally challenging user experience. The “immutable” and “irreversible” nature of many blockchain transactions creates significant friction and risk for users accustomed to the safety nets of traditional banking.

Unlike a mistaken credit card charge that can be disputed and reversed with a call to customer service, an error in a crypto transaction is often permanent. This lack of a centralized support system remains a critical barrier that must be overcome before digital assets can be seamlessly and safely embedded into mainstream consumer applications.

Conclusion The Seamless Integration of Finance

The analysis showed that the embedded finance surge has fundamentally reshaped how consumers interact with financial services, a shift driven by unparalleled convenience and powerful strategic benefits for brands. This transformation was not isolated; it was accelerated by parallel trends, including a more open regulatory environment and the rise of automated agentic finance, which added layers of intelligence and value to integrated experiences. The continued fusion of finance into our daily digital lives appears inevitable, but its ultimate success depended on the industry’s ability to build experiences that are not only seamless but also deeply trustworthy and intuitively user-friendly.