The silent transformation of the global financial architecture has reached a point where the most successful transaction is the one that the user never actually perceives as a payment. In the current digital economy, the most sophisticated technology is often the kind that remains entirely unnoticed, operating quietly behind the interface of popular applications. This principle is revolutionizing the financial sector through embedded finance, which involves the direct integration of banking and payment services into non-financial platforms. No longer a standalone destination, financial tools are becoming the invisible connective tissue within the software used for work, travel, and socializing. This structural shift moves the center of value away from the transaction itself and toward the overall user experience, positioning Software-as-a-Service (SaaS) brands as the new gatekeepers of the financial world.

The Seamless Integration of Finance into the Digital Experience

Embedded finance represents a departure from the traditional siloed approach to banking, where users had to exit one environment to complete a financial task in another. By weaving credit, insurance, and payment processing into the fabric of daily-use apps, businesses are effectively eliminating the “payment wall” that once interrupted the consumer journey. This integration allows a ride-sharing app to handle payments automatically or a retail platform to offer instant financing at the point of sale without requiring a separate credit application. The result is a frictionless ecosystem where the financial component is a supportive feature rather than a primary obstacle.

As digital native companies continue to dominate market share, the demand for integrated financial services is accelerating. These platforms leverage deep pools of user data to offer highly personalized financial products at the exact moment of need. For instance, a logistics platform might offer specialized insurance to a driver exactly when a high-value shipment is accepted. This level of contextual relevance is something traditional banks struggle to replicate, as they often lack the real-time behavioral data that SaaS providers possess. Consequently, the relationship between the consumer and the financial service is becoming defined by the platform’s utility rather than the bank’s brand.

From Visible Products to Background Infrastructure

Historically, financial services were marketed as distinct, branded products that required active engagement from the consumer. Individuals and businesses sought out specific banks for credit cards, checking accounts, or loans, and the physical card or digital wallet was the primary focus of the interaction. However, the industry has undergone a massive evolution toward an outcome-oriented model. In this landscape, users are not looking for a better card in isolation; they are searching for a specific result, such as the automatic reconciliation of a business expense or instant access to investment liquidity. This shift has turned payments into background infrastructure, where value is measured by how effectively a transaction facilitates a broader digital journey.

The move toward infrastructure-based finance from 2026 to 2028 is expected to redefine the competitive landscape for traditional lenders. As the act of paying becomes a secondary byproduct of a business process or social interaction, the visibility of the underlying bank diminishes. This means that while regulated institutions still provide the necessary balance sheets and compliance frameworks, they are increasingly operating behind the scenes. The primary interface belongs to the software provider, which captures the user’s attention and loyalty, while the financial institution provides the high-performance plumbing that makes the “invisible” experience possible.

The Strategic Role of Workflow and Behavior

Removing Friction Through Workflow Integration

In the B2B sector, embedded finance is fundamentally altering how companies manage their operations by turning financial instruments into workflow infrastructure. Modern platforms illustrate this trend by embedding payment capabilities directly into expense management and accounting software. Here, the primary value is not merely the ability to spend money, but the automated reconciliation, policy enforcement, and real-time document flow that the transaction triggers. By removing the administrative burden of manual accounting, embedded finance allows professionals to focus on their core objectives. The actual act of payment becomes a nearly imperceptible part of a larger, automated business process that saves time and reduces human error.

Transforming Consumer Behavior Through Fluid Liquidity

On the consumer side, embedded finance acts as a bridge between previously siloed financial behaviors, such as investing and daily spending. Innovative platforms now allow users to spend directly from their investment balances via embedded cards, effectively removing the traditional barriers and wait times associated with moving money between different accounts. This integration encourages users to maintain higher balances within a single ecosystem, as their capital remains fluid and accessible at all times. By making liquidity instant, these platforms reshape the user’s relationship with their wealth. The financial tool becomes a natural extension of an investment strategy, fostering deeper brand loyalty through sheer convenience.

Navigating Contextual Resilience and Global Variations

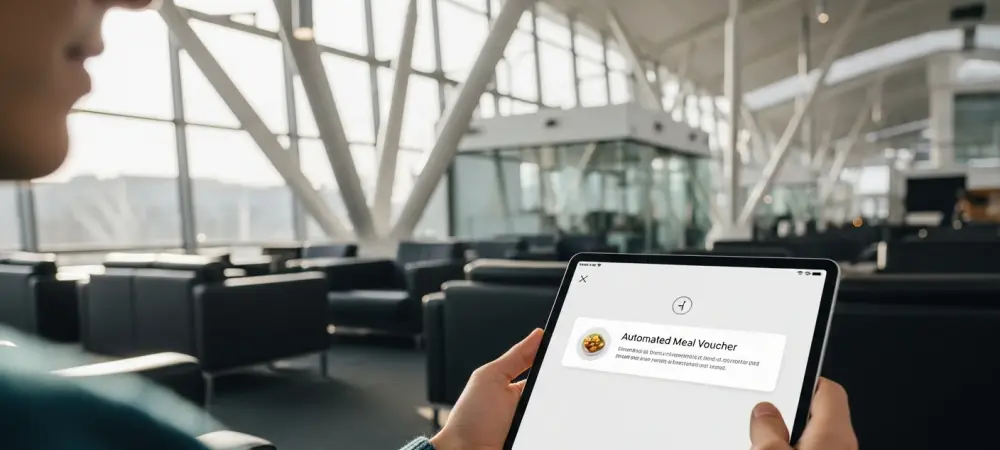

The most powerful applications of invisible payments often emerge in moments of high stress or specific social contexts where traditional banking fails to meet the immediate need. For example, the use of instant virtual cards provides immediate relief to passengers during travel disruptions, such as flight cancellations. In this scenario, the payment is perceived as a gesture of care and support rather than a cold financial transaction. Furthermore, as messaging apps integrate payment features, money movement begins to inherit the social context of a conversation. While regional regulations and infrastructure vary globally, the trend is clear: payments are becoming an emotional and contextual tool that adapts to the user’s environment.

The Future of Financial Gatekeeping and Innovation

The landscape of financial services is heading toward a future where digital product brands, rather than traditional banks, own the primary customer relationship. As payments become a quiet feature of a larger ecosystem, the role of regulated financial institutions will continue to shift toward providing high-performance, behind-the-scenes infrastructure. We are likely to see the rise of super apps where insurance, lending, and payments are suggested proactively based on predictive user data. Technological advancements in artificial intelligence and distributed ledger technology will likely further automate these processes, making financial decisions more autonomous and the underlying transactions even more invisible to the end user.

This evolution will also necessitate a shift in how financial health is monitored and managed. When transactions are invisible, there is a risk that users may lose track of their spending habits or financial commitments. To counter this, future innovations will likely focus on “smart visibility,” where AI-driven dashboards provide high-level insights without reintroducing the friction of manual payments. The gatekeepers of the future will be those who can balance the convenience of invisibility with the transparency required for responsible financial management, ensuring that the user remains in control even as the mechanics of the transaction fade away.

Strategic Takeaways for the Embedded Era

The transition toward invisible payments offers significant opportunities for both businesses and consumers. For SaaS providers, the goal should be to design ecosystems where finance feels like an effortless component of the user journey rather than an external requirement. Businesses should prioritize outcome-driven financial tools that automate manual tasks and integrate deeply with existing data structures. This approach not only improves operational efficiency but also creates a more “sticky” product that users are reluctant to leave. Success in this era depends on the ability to treat finance as a feature of the user experience rather than a separate product category.

Consumers should look for platforms that offer fluid access to their capital across different services, prioritizing those that provide the most seamless integration with their lifestyle or business needs. For financial institutions, the strategy involves a pivot toward becoming an infrastructure-as-a-service provider. By offering robust APIs and high-uptime settlement layers, traditional banks can remain relevant in an era where they no longer hold the front-end relationship. The key to winning in this market is not to market the payment itself, but to perfect the experience that the payment enables, ensuring the financial layer serves the user’s ultimate goal without interruption.

The Permanent Shift Toward Experience-Led Finance

The rise of embedded finance marked the definitive end of the era where the standalone payment product reigned supreme. By shifting the focus from the instrument to the outcome and from the transaction to the experience, digital platforms successfully captured the value that traditional banks once held. As these services became more integrated and contextual, they turned into indispensable components of the modern digital lifestyle. The industry recognized that the most powerful financial tools were the ones the user barely noticed because they functioned so perfectly within the fabric of their daily routine. This evolution proved that the future of finance was not found in better cards or faster apps, but in the complete disappearance of the payment process into the background of human activity.

Ultimately, the strategies adopted during this transition redefined the relationship between technology and capital. Companies that prioritized the user journey over the transaction fee emerged as the leaders of the new financial order. They demonstrated that by making liquidity instant and invisible, they could foster a level of trust and loyalty that traditional banking models could not achieve. The shift toward experience-led finance was not merely a technological upgrade; it was a fundamental change in how value was perceived and delivered across the globe. As financial layers became entirely silent, they paradoxically became more influential, shaping the way people lived, worked, and interacted in a fully connected world.