The End of the Traditional ID: Ghana’s Leap into the Global Financial Grid

A single piece of polycarbonate identification has officially transcended its role as a mere residency permit to become the master key for international financial markets for millions of Ghanaian citizens. The activation of the digital wallet for the Ghana Card is not just a technical update; it represents a fundamental shift in how the nation interacts with the global economy. By merging biometric data with international payment capabilities, the country bypassed traditional banking hurdles and empowered its population.

This initiative allows individuals to carry financial independence in their pockets, effectively turning a state document into a portable bank. Such a transition signals the end of the plastic era and the beginning of integrated digital sovereignty.

Bridging the Gap Between Identity and Financial Inclusion

The National Identification Authority (NIA) designed this evolution to tackle the persistent issue of financial exclusion that once sidelined a large portion of the population. Historically, the absence of verifiable identity barred many from formal banking services and credit opportunities. The Ghana Card now serves as the primary authentication tool for electronic payments, aligning with rigorous global standards. This strategic alignment positioned the nation as a frontrunner in the African digital economy, ensuring that national identity acts as a gateway to domestic stability.

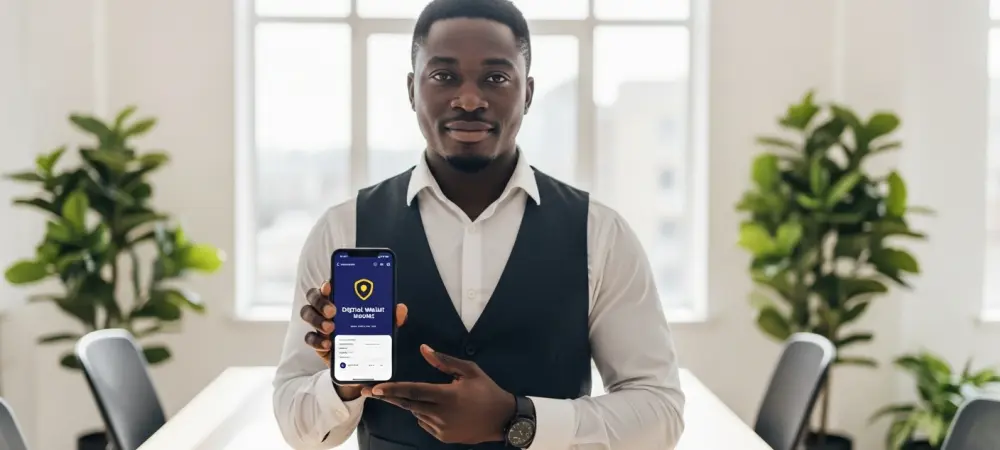

From Identification to Transaction: Core Capabilities of the Digital Wallet

The new functionality transformed the Ghana Card from a passive document into an active financial instrument. Users link their national IDs directly to bank accounts, allowing the card to function as a debit tool for ATM withdrawals and online purchases. Significantly, the authorization for payments extends to approximately 200 countries and territories. This integration complements the card’s existing e-passport capabilities and biometric functions, creating a consolidated platform for money management.

Visionary Implementation and the New Economic Framework

Executive Secretary Yayra Korku Deku and the NIA spearheaded this transition as part of a broader push toward a digitized economic framework. Consolidating these services into a single platform reduced fraud and streamlined administrative overhead. To sustain this high-tech infrastructure, a revised fee structure remained in place. First-time applicants under 25 paid 30 Ghanaian cedis, while card replacements were set at 200 Ghanaian cedis. These tiers ensured accessibility while funding the security protocols required for international interoperability.

How to Activate and Navigate the Global Digital Wallet

Citizens managed these features through the MyCitizen App, which served as the primary interface for tracking transactions and verifying credentials. For those without internet access, USSD codes provided a vital offline alternative for wallet management. Once the authentication steps synced biometric data with financial records, the card functioned at any global merchant. This system empowered the workforce to explore new investment avenues and solidified the digital infrastructure. The government fostered a climate where every citizen secured their financial future through a unified digital identity. This move successfully integrated the domestic market into the global financial ecosystem.